Do You Work Directly With the MA RMV?

Is there a faster way to register your car in Massachusetts? If you're like most car buyers or dealership customers in Massachusetts, you've probably faced the long lines and red tape of the RMV...

Read more

Is My Child Covered If They Just Got Their Massachusetts Learner's Permit?

What’s the first thing I need to know about insurance and learner’s permits in Massachusetts? As soon as your child gets their learner's permit, you're likely asking: “Are they automatically...

Read more

Do I Have to Pay My First Year’s Home Insurance If I Have Escrow?

Why is my mortgage payment going up after the first year? Why did I have to pay the first year’s premium if I have an escrow account?We’re going to clear up the confusion around who pays what,...

Read more

Insurance Claim Denied? Here Are Your Options (Fight Back and Win!)

Has your insurance company recently denied your claim, leaving you frustrated and unsure what to do next? Do you know that a denial isn’t the end of the road — and that you may have more power...

Read more

14 Ways to Save Money on Homeowners Insurance (Massachusetts Homeowners Save $500+

We hear this often, why does homeowners insurance seem to get more expensive every year? And how can Massachusetts residents reduce their premiums without cutting corners on coverage? If you’ve...

Read more

Personal Liability Insurance: What Happens When Someone Gets Hurt on Your Property

What happens if someone trips, slips, or falls on your property? Whether it’s a friend, delivery driver, or neighbor, accidents can happen fast—and they’re almost always unexpected. One minute you...

Read more

Insurance Adjusters: What to Expect and How to Get a Fair Settlement

What’s going on behind the scenes after you file an insurance claim? After a car accident, natural disaster, or property loss, you're likely feeling overwhelmed—and then, an insurance adjuster...

Read more

Do You REALLY Need Photos for Insurance Claims?

A Picture is Worth A Thousand Words in Insurance Claims Imagine this: a Boston homeowner returns from vacation to find a burst pipe has flooded their basement. They panic, call the plumber, and...

Read more

🏡 What Homeowners Insurance Doesn’t Cover — And What You Can Do About It

Do you think your homeowners insurance protects you from everything? What if the biggest risks to your home aren’t actually covered? In this article, you'll learn what homeowners insurance...

Read more

Money-Saving Homeowner Secrets: 7 Discounts Most Beginners Miss

Are you paying more than necessary for your homeowners insurance? Have you reviewed your policy to make sure you’re getting all the discounts you qualify for? This article breaks down the most...

Read more

Smart Homeowner’s Guide: 7 Steps to Save Thousands on Insurance

Are you a new homeowner in Massachusetts, overwhelmed by the process of shopping for homeowners insurance? “Homeowners insurance isn't just a formality—it's your financial safety net,” says the...

Read more

Does Homeowners Insurance Cover Floods?

Understanding Your Homeowners Insurance Coverage When it comes to protecting your home, the assumption that your homeowners insurance covers every possible event can be misleading.Many homeowners...

Read more

The Psychology Behind Underinsurance: A Shared Experience

A Shared Experience of Hesitation Have you ever found yourself thinking, "I really need to get life insurance," yet never quite following through? You're far from alone. Many of us have been in...

Read more

View more

Think your homeowners insurance has you covered if a flood hits your neighborhood? What if we told you that it probably doesn’t — and you won’t find out until it’s too late?

Commercial insurance policies are complicated. At Vargas & Vargas, we know small business owners are focused on running their businesses. You don’t always have the time to pour over commercial insurance policies in detail. Today, we will make a few key points that you should consider as we move forward in 2021.

Question 2: Do you know whether your building has a master condo policy — or if you’ve been quoted homeowners (HO3) policy by mistake?

Some people purchase condos in Dorchester, MA, as investment properties to rent out and generate income. If this is your situation, it’s important to take extra precautions when insuring your property. Vargas & Vargas Insurance can provide the advice you need to determine the best course of action for protecting your condo investment.

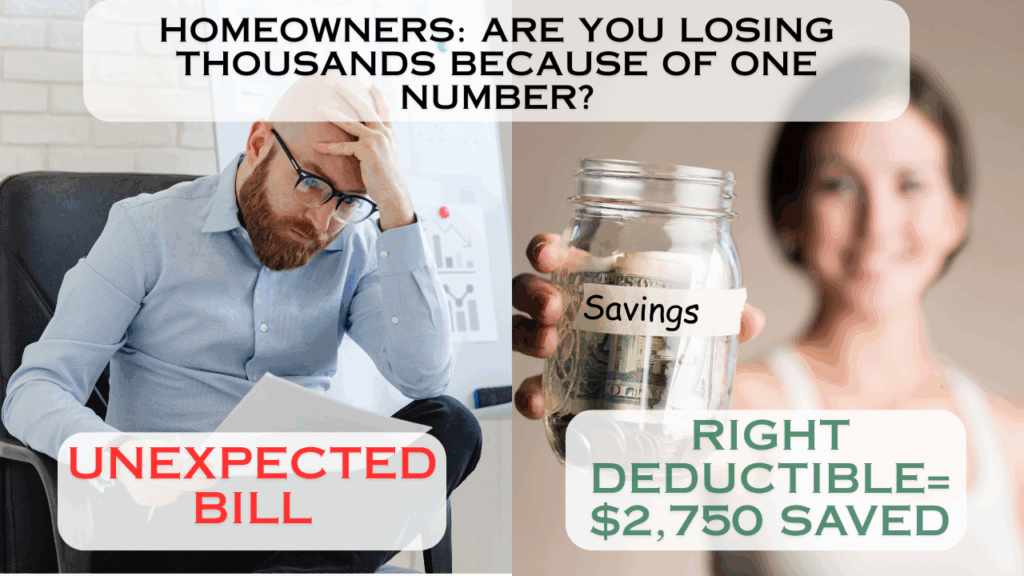

Question: Not sure if your homeowners insurance deductible is too high or too low? Question: Are you paying more than you should each year just because you picked the “default” deductible? In this article, you’ll learn how to choose the right homeowners insurance deductible based on your home, budget, risk level, and financial goals. We’ll walk you through the different types of deductibles, show how they impact your premium, and help you confidently select the amount that saves you money without exposing you to unnecessary risk.

Have you been told your policy is with a “non-admitted” carrier and wondered if that’s a bad thing?

You just bought your home for $675,000—so why is your insurance company saying it’s only worth $450,000?

Think your homeowners insurance covers everything?

Have you been denied home insurance because of your property’s age, location, or past claims?

Have you just been handed the keys to a “new-to-you” car and wondered, “What paperwork will the RMV need so I’m not hit with sales tax?”

If you’re a homeowner in Massachusetts, you know protecting your home is non-negotiable. But finding the right insurance policy? That can feel overwhelming. With dozens of carriers, coverage levels, and price points, how do you know which one is best?

Have you discovered chewed wires or insulation in your Massachusetts home—and panicked about whether insurance would help?